Source: Miles Cole

Download full data on how institutions’ finances compare

People look at organisations making a surplus and think ‘profit’; they think you’re OK. They don’t understand that you need surpluses to fund the future

Sitting on growing surpluses, enjoying increasing income and paying their leaders handsomely: at first glance, such facts might make the UK’s universities appear to be rather flush and an attractive target for politicians seeking post-election spending cuts.

But with the sector grappling with tuition fees capped at £9,000 a year, ever more demands for significant capital investment and mounting staff costs, are universities really in robust financial shape?

Times Higher Education’s annual financial health check, using university data collated by the accountancy firm Grant Thornton, suggests that 2013-14 gave institutions a chance to steady themselves after the upheaval caused by the introduction of £9,000 fees the previous year.

During 2013-14, UK universities generated surpluses totalling £1.2 billion before exceptional items were considered, up 12.6 per cent year-on-year.

As a percentage of total income – a good measure of financial health – this stood at 3.9 per cent, up from 3.7 per cent the previous year, after two successive years of decline.

Total sector income in 2013-14 came to £30.7 billion, up 5.7 per cent on the previous year, or £30.6 billion if the private institutions ifs and Regent’s University London are excluded.

For David Barnes, a partner and head of higher education at Grant Thornton, the surpluses “support the view that the sector as a whole is financially sound”.

However, with major challenges ahead, Barnes questions “whether surpluses are sufficient in the medium to long term for all institutions to be able to maintain and develop their capital estate and, in some cases, to fully implement ambitious investment plans”.

The overall picture also masks significant variation in individual performance. Of 160 institutions included in THE’s analysis, 143 were in surplus before exceptional items, and 80 enjoyed a surplus equivalent to 4 per cent or more of their income.

On this measure, the top performers were small institutions and post-92 universities. Fifteen institutions had surpluses in excess of 10 per cent of income, among them Norwich University of the Arts (18.4 per cent), Liverpool Institute for Performing Arts (16.2 per cent), the University of Huddersfield (15.2 per cent) and Edge Hill University (15.1 per cent).

Older, larger institutions tended to fare less well on this measure, with the University of Bath (7.7 per cent) emerging as the top performer.

Among the Russell Group of research-intensive universities, Imperial College London (6.9 per cent), the University of Leeds (6.6 per cent) and the London School of Economics (6.5 per cent) achieved the strongest results.

Meanwhile, 17 universities were in deficit, compared with 19 last year. Three of them are Russell Group members: King’s College London, the University of Cambridge (both 0.4 per cent) and the University of Exeter (0.6 per cent).

But their books were well balanced compared with the £9.7 million deficit at City University London (5 per cent of income) and the £13.3 million shortfall at the University of Reading (5.5 per cent), both of which were attributed to planned investment in staff and infrastructure.

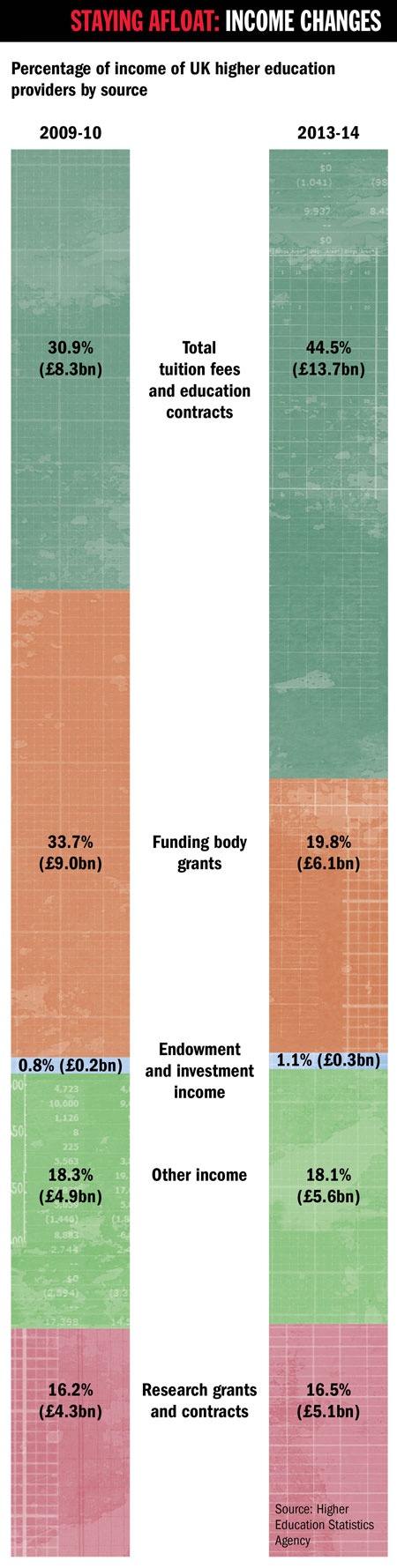

Phil McNaull, director of finance at the University of Edinburgh and deputy chair of the British Universities Finance Directors Group, said the overall figures showed that universities had responded effectively to the switch from majority public funding to majority private funding (see ‘Staying afloat: income changes’ graphic).

Total funding council grants fell by 13.5 per cent during 2013-14, to £6.1 billion.

But McNaull says that surpluses should not lead people to think that things were now rosy.

“People look at organisations making a surplus and they think ‘profit’; they think you’re OK,” he says. “They don’t understand that you need to make surpluses to fund the future.”

And the future does hold challenges for the sector. Chief among them is the demand for capital spending, which is already evident on a walk around most university campuses: the growth in the number of shiny new buildings reflects how improving the student experience has become a priority amid an increasingly competitive recruitment environment.

According to the THE-Grant Thornton analysis, the sector spent £3.7 billion on capital projects in 2013-14, an increase of 7.8 per cent year-on-year.

Sue Holmes, director of estates and facilities management at Oxford Brookes University and chair of the Association of University Directors of Estates, does not foresee any let-up in investment as student recruitment gets ever more competitive.

“I don’t think this will go away,” she says. “We know that if we ease up on investment, we build up a backlog, which is even more challenging to deal with.”

However, Holmes adds, directors of estates recognise that a lot of future spending may be focused on the refurbishment of existing buildings rather than new construction, and she acknowledges that there is pressure to raise income by hiring out premises when they are not being used by students or staff.

The other key financial challenge is staffing costs, which totalled £16.3 billion for 2013-14 in THE’s data, up 6.1 per cent on the previous year. This accounts for 53 per cent of total university income, and Barnes expects this to rise “in the medium term”, particularly as a result of employers having to increase their contributions to the Universities Superannuation Scheme.

Again, there was widespread variety in universities’ performance. For some, staffing costs accounted for the majority of their income, such as Abertay University (65.4 per cent) and King’s College London (62.4 per cent).

For other institutions, the proportion was much smaller. Personnel costs accounted for 19.4 per cent of income at the University of the Highlands and Islands and 43.2 per cent at the University of Cambridge.

Institutions are wrestling with these issues and more at a time of continuing political uncertainty, with Labour proposing to make universities more dependent on government funding via a reduction in annual tuition fees to £6,000.

We know that if we ease up on investment, we build up a backlog, which is even more challenging to deal with

Meanwhile, because of inflation, the real terms value of £9,000 tuition fees has declined in recent years.

The impact of inflation on income is an important factor for Susan Price, the outgoing vice-chancellor of Leeds Beckett University.

The institution has taken care to expand its reserves in recent years because, Price says, it needed to build its “financial strength and depth”.

In 2013-14, it made a surplus of £24.1 million, equivalent to 12.1 per cent of income.

“We have invested significantly in our estate and in new posts, and we do have plans to continue to invest,” Price says. “We are developing our reserves as a buffer against, at very best, no increase in funding, and to make sure that we are able to invest without further significant borrowing.”

But how might institutions without large financial reserves be able to underwrite planned expenditure in the future?

One answer is through making more efficiencies. A recent report on the subject for Universities UK led by Sir Ian Diamond, principal and vice-chancellor of the University of Aberdeen, suggested the possibility of replacing automatic pay rises linked to length of service with performance-related rewards.

However, with more than £1 billion of efficiency savings having been made across the sector in the past three years, there are questions about how easy it will be to cut further.

Another option is borrowing, which stood at £7.3 billion across the sector in 2013-14, according to THE’s data. This was up 3.3 per cent on the previous year.

The University of Manchester, which issued a £300 million bond in 2013, had the largest debts, totalling £421.0 million – equivalent to 47.5 per cent of its annual income.

Three other institutions – the University of Bristol, Imperial College and Exeter – had borrowing exceeding £200 million.

Seven institutions had debts exceeding two-thirds of the value of their annual income: Queen Margaret University (161.7 per cent), the University of Worcester (93.1 per cent), the University of Surrey (81.6 per cent) and Glasgow School of Art (77.0 per cent), plus Oxford Brookes (75.3 per cent), Bath (73.5 per cent) and Exeter (67.7 per cent).

All these issues are reflected in Hefce’s report on the sector’s 2013-14 finances, Financial Health of the Higher Education Sector: Financial Results and TRAC Outcomes 2013-14, which finds a “financially sound position overall”. But it says that there “continue to be significant variations in the financial performances of individual institutions across the sector”.

According to Hefce’s analysis – sourced from institutions’ financial returns to the funding council as well as data from the Higher Education Statistics Agency – capital investment at Hefce-funded institutions in England rose in 2013-14, up 23 per cent to £3.3 billion. To help fund that spending, Hefce says, the sector used £1.6 billion from its cash reserves and borrowed an additional £501 million.

“This caused total sector borrowing to rise to £6.7 billion at the end of July 2014 (equivalent to 26.3 per cent of income),” the funding council adds.

Hefce continues: “Without increased surpluses and continued government support, there is a risk that the sector will be unable to deliver the scale of investment required to meet student demands, build capacity and ensure that the sector can remain internationally competitive.

“Government support also fosters confidence to others to continue to invest in the sector, including willingness of banks to lend money, although the sector’s capacity to lever in funding from other sources, including additional borrowing, is limited and may not be sufficient to meet the sector’s long-term investment needs.”

In the report, Hefce provides data from returns that universities have submitted about their costs for the Transparent Approach to Costing. In the past, concerns have been expressed about the accuracy of Trac data but Hefce says the data undergo checks and that its validation processes mean that “we can be assured that the sector data [are] robust at the required level of materiality”. A table listing the Trac figures says that in 2013-14 English universities made a slim surplus of £219 million on teaching home and other European Union students. This equates to 2.1 per cent of income from home/EU students.

But on teaching overseas students, that figure is much bigger: universities had a surplus of £977 million, or 26.8 per cent of income from international students.

As to why English universities would need to make such a hefty surplus on the backs of their overseas students, one clue might lie in the figure listed in the table’s next column, on research. There, English universities returned a huge £2.4 billion deficit, equivalent to 35.5 per cent of research income.

Bob Rabone, chair of the British Universities Finance Directors Group and chief financial officer at the University of Sheffield, says the Trac figures show “how increasingly difficult funding research is becoming. Only those institutions that are producing surpluses on overseas students are able to fund [the cost of] taking on research awards.”

He continues: “Doing research is expensive stuff. Those numbers show you that much more clearly than anything else we have…That’s the price we’re given and we’d rather do the research for the funds available and try to make up the gap. That doesn’t mean to say that it’s either sustainable long term or sensible.”

So why is there such a large gap between funding for research and the full economic cost of conducting research? Rabone points to “Wakeham slicing”. In 2010, a report for the government by Sir William Wakeham, former vice-chancellor of the University of Southampton, said that universities should make annual efficiency savings of 5 per cent from the indirect costs of research – areas such as libraries and administration – for the following three years. Provision for indirect costs in grants awarded by the research councils should also be reduced by 5 per cent a year, he said.

Without surpluses and government support, there is a risk the sector will be unable to deliver the investment required to meet student demands

Rabone argues that the full economic costs of research have never been covered “even in the UK, and European rates are lower than the UK rates”. And the deficit has grown, he says, because universities are “doing more European research”.

In terms of the general picture on finances presented by Hefce, Rabone sees a “slight recovery in 2013-14 because of the student changes [increased numbers] and continued calmness – similar level of surplus, similar level of growth as previous years”. In his view, the sector’s level of borrowing is “of note, but not of concern”.

Of the funding council’s report, Andrew McGettigan, author of The Great University Gamble, says that “although the sector appears stable, individual institutions are facing difficulties, and Hefce notes that it is too early to assess the funding changes brought about in 2012”. Meanwhile, accounting changes (bringing infrastructure contracts with private operators, including those covering student accommodation, on to universities’ balance sheets) “may impact on the perceived indebtedness of the sector”, according to Hefce.

“Hefce appears most concerned about the sector’s ability to generate and maintain the surpluses necessary to fund investment given the decline of capital grants,” McGettigan says. “In the medium term, this will have knock-on implications for the range of activities in which universities currently engage.”

Highlighting Hefce’s prediction that some institutions “are likely to face difficult decisions”, McGettigan argues that universities need to do more to improve “governance and managerial arrangements” so staff and students are not excluded from involvement in decisions.

For the future, the key element of uncertainty remains the lifting of the cap on student numbers this autumn, which will allow institutions to recruit as many students as they wish.

Some universities could seize the opportunity to expand, potentially at the expense of other institutions. For universities that choose to grow, the increase in student numbers could put yet more pressure on teaching and infrastructure costs.

The cap “had previously provided some degree of income protection”, Barnes says. “In the medium term, we expect the funding changes to create wider variations in operating results across institutions, with there being winners and losers depending on the ability of institutions to appropriately adapt and respond to change.”

If tuition fees are not allowed to rise above the current £9,000 ceiling, Chris Hearn, head of education at Barclays Corporate, predicts that some leading universities might aim to widen their intake to boost their income.

“What if you’re a middle-ranking or lower-ranking research institution that suddenly finds you have got some of the top-ranking universities after your student base and, maybe, your researchers?” he asks. Such a scenario could mean that institutions in “the middle could be squeezed hardest”.

More broadly, McNaull expects surpluses to “start to ease off” in the next two to three years as rising staff costs start to bite. He too cites the capping of fees at £9,000 as a concern.

“Some of our costs are moving faster than inflation,” he says. “If income is capped and costs are rising, the squeeze is on.”

In this situation, to reduce the risk of the sector’s being targeted for funding cuts, universities must clearly spell out the challenges they face and communicate the rationale behind accumulating surpluses.

“The danger is that people see [the sector’s] resilience as something they can continue to press on; but if you continue to pull an elastic band, at some point it will snap,” McNaull says. “I would prefer to see a steadier approach to sustaining universities and their funding, rather than just assuming that everything will be all right. If you have to make the same money go further each year, something eventually will have to give.”

A hard habit to break: reliance on non-EU fees continues growing

UK universities are becoming increasingly reliant on international students, which now provide more than 12 per cent of their total income.

Tuition fees paid by overseas learners stood at £3.7 billion in 2013-14, a rise of 10.9 per cent year-on-year, according to institutional accounts.

Some institutions rely heavily on international students, among them the University of London and the University of Sunderland, both of which drew 35.6 per cent of income from this source.

Several institutions based in the capital receive a significant proportion of their income from international tuition fees, including the University of the Arts London (32.6 per cent), the London School of Economics (31.1 per cent) and City University London (28.1 per cent).

But a number of universities outside the capital were also major beneficiaries, including Heriot-Watt University (27.2 per cent), the University of St Andrews (23.2 per cent) and Coventry University (23.1 per cent). (Note that, in some cases, these figures may include income from other international education activities.)

However, many other institutions draw only a very small proportion of their total income from international tuition fees.

Bob Rabone, chair of the British Universities Finance Directors Group, says that the Higher Education Funding Council for England’s analysis of data from Transparent Approach to Costing returns suggests that the market in overseas students is “a high-margin business with increasing prices – and at some point you’re at risk of overpricing what you supply compared to the rest of the market”.

Are the fees of overseas students providing a cross-subsidy for English universities to carry out research? According to Rabone, the Trac figures show that overseas fees are “the biggest single component which tries to help” and “clearly [are] part of the sustainability of the sector”.

Hefce’s verdict in its report is that the data show that “surpluses on non-publicly funded teaching [overseas students] and other activities are insufficient to support the shortfall on research, and the increasing sustainability gap for 2013-14 reflects the fact that the sector is not generating enough income to finance all its activities and investment”. In future, some institutions may look to recruit more overseas students to help maintain surpluses, predicts David Barnes, a partner and head of higher education at Grant Thornton.

“Should Russell Group institutions, for example, seek to increase overseas numbers significantly, this is likely to be at the expense of other institutions, a number of which may have become reliant on this income stream,” he warns.

Register to continue

Why register?

- Registration is free and only takes a moment

- Once registered, you can read 3 articles a month

- Sign up for our newsletter

Subscribe

Or subscribe for unlimited access to:

- Unlimited access to news, views, insights & reviews

- Digital editions

- Digital access to THE’s university and college rankings analysis

Already registered or a current subscriber? Login